How to open a bank account as a foreigner

Our guide shows you the necessary steps to open a bank account as a foreigner in Germany.

A review of the best German bank accounts in 2026 for expats. One of the first things you should do when moving to Germany is to open a checking account with an IBAN number. You need it to pay our rent and to receive salaries. I have a selection of the best checking accounts for foreigners in Germany in this review.

Too long to read? Here are my picks: For a quick setup (all you need is your phone) and full English language support, use *Wise. For a better long-term price and if you are fine with a German app and website and some English support on the phone use *1822direkt or Ing Diba.

It is very hard to live in Germany without having a checking account or current account, a so-called Girokonto. You need it to pay your rent, receive salaries, to get a mobile or an internet contract.

The most used payment method in shops and restaurants in Germany besides cash is the debit card. The debit card is connected to your checking account. Most German banks offer online bank accounts either through an app or online banking. Some banks are brick-and-mortar banks with branches and some are online banks only. Checking account fees vary between 0.- and up to 20.- Euros per month.

Payments are debited the same day or a couple of days afterward. The banks usually offer you a bank overdraft called Dispositionskredit or Dispo if you have a regular income.

The Dispo might only work if you withdraw on ATMs issued by the bank itself and might not work at all if outside Germany.

Do not rely only on credit cards for payments as they are not always accepted in Germany. You probably want to have a debit card as your main card and always carry some cash.

Don't be surprised if smaller shops and restaurants in Germany ask you to pay cash and do not accept any other form of payment. 😨

Most German credit cards and debit cards have a contactless payment feature. Contactless payment is possible without entering your pin for smaller sums, usually below 40.- Euro. The banks charge fees depending on which ATM you withdraw money but some banks do not charge withdrawal fees at all. Many German bank accounts can be connected to Apple or Google pay.

Credit cards in Germany are not used for deferring payments the same way as in the US or other countries. Germans use consumer credits (Verbraucherkredit) for deferring payments or the checking accounts' overdraft when ends don't meet at the end of the month. Generally, it is frowned upon to buy smaller consumer goods like a TV on credit in Germany.

Please note that all checking accounts in this review are for personal use only. Have a look at my best free bank accounts for small businesses and freelancers if you are doing business in Germany and need a separate business account.

The standard for wiring money to another person or company in Europe is a SEPA transfer using IBAN and BIC numbers. This is called Überweisung. A SEPA transfer often has an option for an instant transfer: in this case the money is transferred within minutes, otherwise it takes up to 2-3 days for the money to be deposited in the other bank account.

Companies asking for your IBAN to direct debit from your bank account is very popular and often the only option for recurring payments like phone or gym contracts. Direct debit in Germany is called Lastschrift or Lastschriftverfahren. Handing out your IBAN to companies for direct debit is considered safe. You can cancel unwanted direct debits in your online banking.

The IBAN identifies your account, the BIC identifies the bank. Those numbers are written on your debit card or in your accounts online area. Instant money transfers which take only a minute are possible for some accounts but money transfers between European countries can take up to several days.

This is the format of a German IBAN number: DE89 3703 0044 0532 0130 00.

Please note that cheques are not used in Europe anymore.

You need to register with authorities once you settle down in Germany. This is called an Anmeldung. Many banks require you to be registered before opening a bank account.

The following banks don't require an Anmeldung source:

A blocked account or Sperrkonto is a special bank account that lets you withdraw only a limited amount of money per month. The money is blocked. The blocked account serves as proof that you have enough money to provide for yourself in Germany and is used by foreign students and visa applicants. A blocked account is a requirement for many German visas.

I recommend *Fintiba as the best blocked account in Germany for visa applications. Deutsche Bank stopped offering blocked accounts as of July 2022 source.

*Coracle's blocked account with a 99.- Euro one-time fee for up to one year might also be an option.

German banks offer basically two kinds of VISA or Maestro cards:

Please note that German debit cards look like credit cards but aren't. You can usually pay anywhere you see the VISA/Maestro sign and many debit cards allow free withdrawals worldwide but you might have issues with the deposit when renting a car and sometimes with payments outside Germany.

Almost every bank in Germany offers at least one credit card added to the checking account but you usually have to pay an additional fee, around 3.- to 8.- Euro per month depending on the bank.

*Barclays offers a free real VISA credit card. You need to have a checking account with another German bank and a German address. It took me 15 minutes to apply for a Barclays credit card online. The Barclays card worked fine on all my travels.

The trick to keeping the Barclays account really free of charge is to configure it so that you always pay off your credit immediately from the checking account at your other bank.

All of the banks listed below offer checking accounts with VISA/Maestro debit cards and most of them offer optional credit or Girocards.

| Name | Remote application* | Service in English | Fees | Support | Checking account | Blocked account | Free for students | For freelancers |

|---|---|---|---|---|---|---|---|---|

| Wise | + | + | -/+ | ? | + | - | + | + *Wise business has no monthly fees |

| bunq | + | + | - | ? | + | - | - | + source |

| DKB | + | - | + | + | + | - | + | - |

| N26 | + | + | + | - | + | - | + | + |

| 1822direkt | ? | - | + | ? | + | - | - | - |

| ING-DiBa | + | - | + | + | + | - | + | - |

*Remote application from another country before you arrive in Germany is possible.

I recommend starting with a *Wise account if you just arrived in Germany. The application process is very easy: all you need is your phone. The Wise app is in English and you get a card and an IBAN number. Wise's prices are fair. There are no fixed monthly costs but it might be cheaper to switch to one of the other banks below in the long term because of withdrawal fees. Wise has nice features like better rates for transfers outside the Eurozone and a modern, international feel that traditional German bank websites don't have.

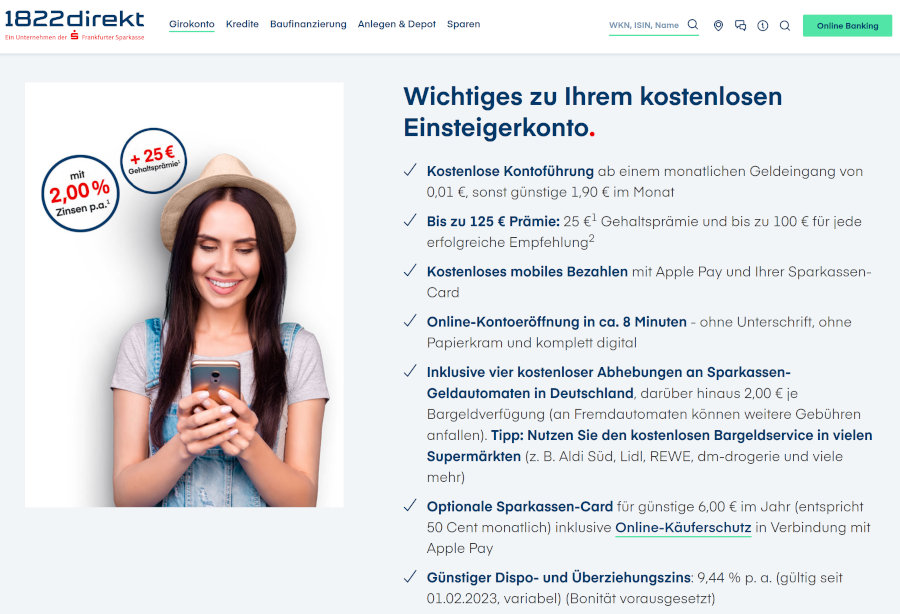

*1822direkt lets you open an account in less than 8 minutes and has no monthly account fees for active users. 1822direkt, with ING, is my recommendation for a German bank. Please note that 1822direkt has a limited amount of free cash withdrawals at ATMs.

*bunq offers full English support and has an easy application process. The bunq Easybank account costs 3.- Euro per month plus 1.- Euro for 5 ATM withdrawals and can be *opened in 5 minutes.

I hear mixed reviews about N26 and personally don't recommend it for longer use but it can make for a great starter bank.

DKB (Deutsche Kreditbank) has a free debit card with free global withdrawals and 24h support. *Apply for the DKB-Girokonto account here. The DKB account is free as long as you have a regular income of at least 700.- Euro per month. Please note that it only makes sense to apply for a DKB account if you have a positive Schufa credit score. You probably don't have any Schufa record at all if you just arrived in Germany. In that case the DKB bank will reject your application. I don't recommend the DKB bank anymore because I think their online banking is not reliably working after the 2023 relaunch and their customer service hotline has long waiting periods. Last time I tried to reach them I had to wait 20 minutes before a human answered the phone.

I hear many good things about ING lately. The ING account, including a VISA debit card, is free if you are under 28 or have a regular income of 700.- per month. Their Visa debit card is free, the Girocard costs 1.- Euro per month source. Free retrievals at 97% of German ATMs source. Open an ING account here.

Note that while some staff might speak English with you, Sparkasse, DKB, ING and 1822 services are generally in the German language only, including online banking and apps. They all have an online area and apps where you can do everything but they look old school compared to bunq and N26. All these banks are fully functional through their online areas and apps only: the last time I had to walk into a Sparkasse branch is like years ago.

What about Sparkasse? Please note that there is a Hamburger Sparkasse, a Berliner Sparkasse and many more but they are different organizations with different conditions. Sparkasse accounts usually have a monthly fee. At the moment of writing the monthly fee for the Berliner Sparkasse is 6.- Euro/month. Opening an account with Sparkasse means walking into one of their branches and talking to a person. I only recommend Sparkasse if you need face-to-face support.

A screenshot of the DKB app. DKB relaunched with a new design in 2023. The DKB account includes a free Visa debit card.

A screenshot of the DKB app. DKB relaunched with a new design in 2023. The DKB account includes a free Visa debit card.  A screenshot of the 1822mobile checking account features. 1822direkt is a traditional bank and can make for a good and low-cost starter bank.

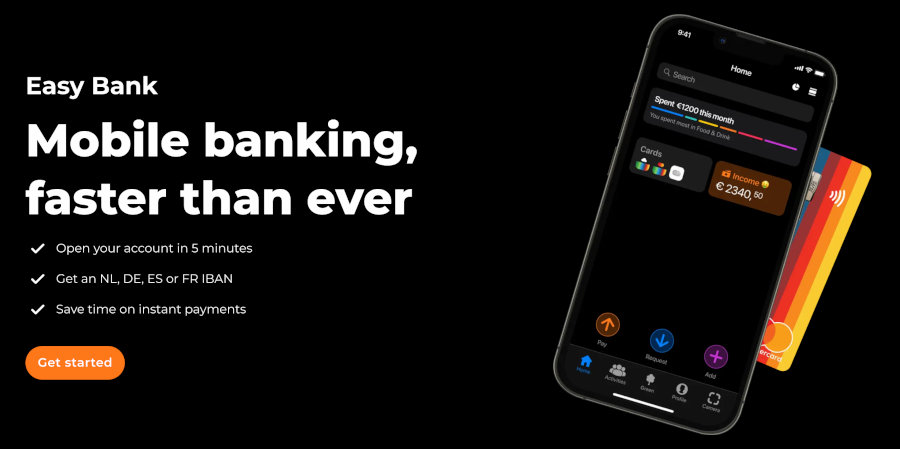

A screenshot of the 1822mobile checking account features. 1822direkt is a traditional bank and can make for a good and low-cost starter bank.  bunq is a Neobank and has a fresher look and feel and a feature set geared towards a more international audience.

bunq is a Neobank and has a fresher look and feel and a feature set geared towards a more international audience.Pros:

Cons:

Fees:

Pros:

Cons:

Pros:

Cons:

Fees:

Pros:

Cons:

Fees:

Opinion:

Pros:

Cons:

Fees:

Pros:

Cons:

Fees:

Postbank migrated their IT systems recently and the resulting problems were so bad for their customers that they even got a reprimand by the official regulatoring institution Bafin source.

The Sparkassen (Berliner Sparkasse, Hamburger Sparkasse) have many branches but I do not see why I should pay a fee for banking if the service is, in my opinion, not better than what online banks are offering.

An easy way to save money in Germany is with a call money account / overnight money account called Tagesgeld. Many banks offer a Tagesgeldkonto free of charge. You can access your money any time simply by transferring money to your checking account. A Tagesgeldkonto pays yearly interests between 1% and 4% on your money. Some banks pay out interest monthly, others yearly. You also get interest payments if you withdraw some of the money.

A selection of call money accounts in Germany:

What to consider when opening a Tagesgeldkonto:

Most German bank accounts allow you to open a bank account using your phone. This usually involves an online video chat with a person to check your identity. That person might only speak German and usually asks you to hold your passport into the camera and read your name, birth date and place, the reason for the call and your passport number. I did this several times and the call duration was usually around 10 to 15 minutes.

Some banks only offer an in-person identity check at the post office called PostIdent.

Prices are not guaranteed. Please check the bank websites for prices.

Our guide shows you the necessary steps to open a bank account as a foreigner in Germany.

An overview of the different types of work visas in Germany. A starter guide for everybody who wants to work in Germany.

What is the procedure when visiting a doctor or a hospital in Germany? How long do I have to wait for appointments? What is the quality of the treatment? What are the cos...

A honest review of Fyrst, Holvi, Kontist, Finom and Wise.

The German Blue Card visa is an option for a permanent residence permit if you are looking to work in mathematics, IT, natural sciences, engineering or human medicine or ...

An independent 2025 review of the best German public and private health insurance plans for singles, couples and families including expat health insurance for visa applic...

How to dial a phone number in Germany.

The best German mobile phone and prepaid plans for expats. A review of Smartmobil, Telekom, Vodafone, Lebara, fraenk.

Public vs private health insurance in Germany for foreigners. Your options and why cheap plans might turn out to be more expensive in the end.

What to pay attention for when applying for private health insurance in Germany.

A guide to getting a German work visa for employees. This visa allows you to work and live in Germany.

Get your money back if you have to cancel your trip because of Corona.

This guide walks you through the all the necessary steps to remotely find a job in Germany, including an overview of the most important job search engines and common appl...

Freelance artists or publishers in Germany are entitled to cheaper healthcare plans via the Künstlersozialkasse (KSK). A step by step guide.

A review of the most useful health apps in Germany.

A step by step guide to get a visa to freelance in Germany.

You can't do all the work at home anymore and need help? Follow this step by step guide to get help covered by your German health insurance.

A step by step guide to find a doctor which speaks your language in Germany based on your ZIP code.

A step by step guide to get your money back if an airline cancelled a flight but does not refund the money.

A honest review of German internet providers and how the pick the best one for your location (and save money).

A step by step guide to register an address in Germany. This is called Anmeldung an necessary to get a tax id, open a bank account or to sign up for health insurance.

The essentials to run a business, consultancy or freelance in Germany: register, get a tax number, healthcare, invoicing, banking.

All about the German student visa, the application process and required documents.

A guide to find the best electricity company in Germany, including comparison websites, and companies with English support.

An introduction into the German tax system for employees.

83% of German households have a private liability insurance. Get protection for as little as 43.- Euro per year. A review for expats including dog liability.

Find an English speaking tax consultant close to your address.

The fastest way to do your taxes in Germany without speaking German. A review of Wiso, Smartsteuer, Wundertax, Sorted.

Introduction into taxes in Germany for consultants, freelancers and other self-employed. This article gives you an overview of the most important types of taxes.

A bureaucratic nightmare with a happy end.

A checklist of steps to do after you found a flat: registration, electricity and internet providers, moving services, useful insurances and warnings of possible scams.